|

| Vincent Murphy Business Broker Owner Panther Equity Advisors |

PANTHER EQUITY ADVISORS -BUSINESS BROKERS

VINCENT MURPHY BUSINESS BROKER-OWNER

Without any small business selling experience, Daniel began searching for a broker who could aide in the process. From his previous work in real estate, Daniel knew of a few options and quickly chose one so he could focus on the bakery while the broker handled the sale. The chosen broker settled on a listing price of $119,000, marketed the business to his network and purchased some advertising but the leads were few and far between.

“It was frustrating because we didn’t know how much work he was putting into finding us a buyer,” Daniel said. “After six months with not one single viewing appointment, we decided to take matters into our own hands.”

A lesson to learn here is that like in most professional industries, there are good and bad brokers and in most cases, a good broker is the best route to a successful exit. Good brokers know how to market your business, qualify buyers and allow you to focus on running your business. But make sure you ask the right questions beforehand, check certifications and discuss his or her marketing plan before you sign with a broker. A few tips to qualifying a business broker:

A lesson to learn here is that like in most professional industries, there are good and bad brokers and in most cases, a good broker is the best route to a successful exit. Good brokers know how to market your business, qualify buyers and allow you to focus on running your business. But make sure you ask the right questions beforehand, check certifications and discuss his or her marketing plan before you sign with a broker. A few tips to qualifying a business broker:- Check the broker’s background: Look for brokers who are committed to the education and credentialing offered by the International Business Brokers Association (IBBA) or other state broker associations. A broker who has obtained the IBBA's CBI (Certified Business Intermediary) designation has met the educational requirements and high ethical standards of the IBBA.

- Ask for details on how the broker will promote your sale: The broker should have a strategy on how they will advertise and market your sale, as well as the steps they will take to maintain confidentiality.

- Ask how many other listings the broker is currently managing and how many businesses they sold last year: If the broker is representing too few listings or hasn’t represented many in the past, it could be a sign that they aren't experienced, motivated or capable.

- Determine how the broker will screen prospects: A big part of the broker's job involves separating the tire-kickers from the serious buyers. Good brokers have an established screening process and usually meet with potential buyers before allowing them to proceed further down the sale path.

Beginning the process on their own, Daniel and Jenny started by creating a listing on BizBuySell.com. They described the bakery in ample detail and provided enough photos for prospective buyers to see both the store and the products they sell. They listed revenue at $440,000 a year and by taking into account profits and assets included in the sale, they listed the business for the same price as the broker. Daniel started receiving immediate interest after placing his ad, earning a half dozen prospects and 3 firm offers within the first two weeks.

“We were very nervous trying to sell the bakery on our own and it was often difficult to find time to show the business while also making sure it was still running smoothly,” Daniel said. “The in person showings ended up being a blessing in disguise however, as I was able to speak in more detail to potential buyers while they visited.”

America’s Best-Selling Businesses: What People Bought in 2015 and How Much They Paid

BizBuySell, the Internet’s largest business-for-sale marketplace, has released its 2015 fourth quarter Insight Report,reporting closed transaction data for the U.S. business-for-sale market. Transactions stabilized in 2015, with the year ending at 3.6 percent below 2014’s record of highest number of reported transactions since BizBuySell first started tracking data in 2007. Full details are included in the BizBuySell 2015 Insight Report, which aggregates statistics from business-for-sale transactions reported by participating business brokers nationwide.

A total of 7,222 closed transactions were reported in 2015, slightly below the 7,494 reported in 2014. At the same time, median sale prices grew in 2015, with sold businesses averaging higher cash flow and higher revenue than in 2014. This suggests that the large influx of business owners holding off on selling until after the recession may have peaked in 2014, leaving a more stabilized market with a strong inventory of high quality, financially healthy businesses that receive higher asking prices. The Florida panhandle led the pack of the highest number of businesses changing hands, followed by the North East metros and then Southern California.

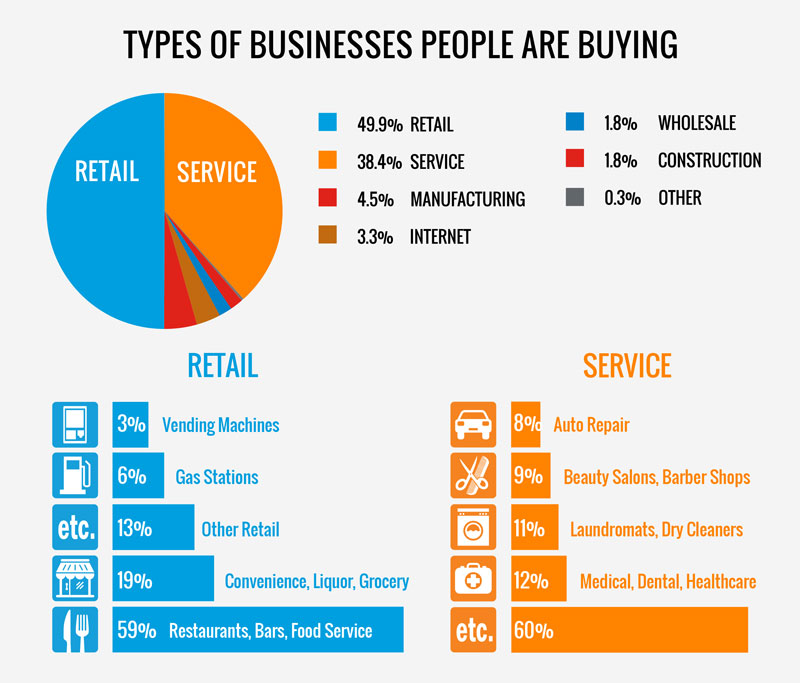

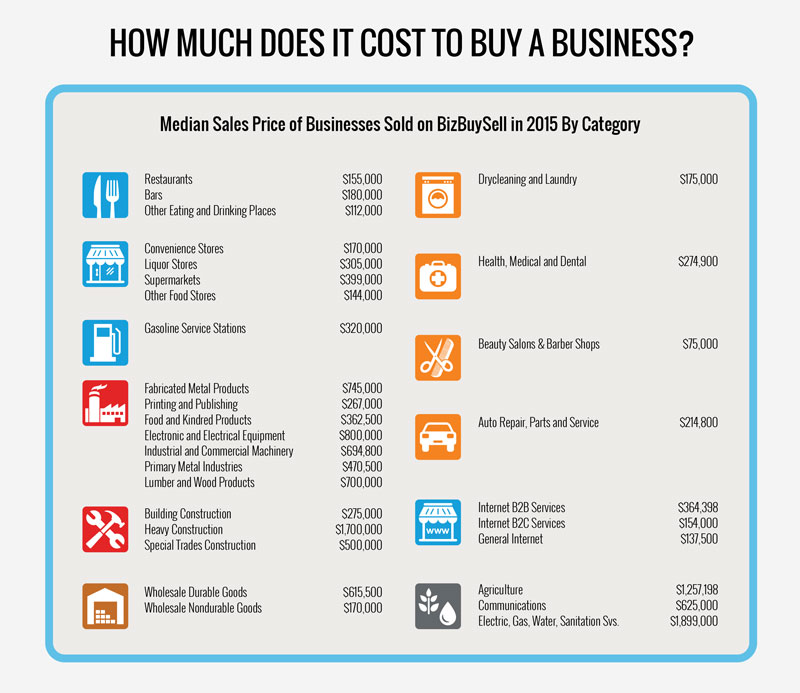

Retail businesses continued to lead the pack as the most popular category of business bought and sold, with restaurants being the most popular sub-category, receiving an average sale price of $155,000. Convenience, liquor and other food stores were close behind, with convenience stores receiving an average sale price of $170,000 and liquor stores receiving an average sale price of $305,000. Service businesses are the second most popular category, with medical, dental and health services being the most popular sub-category, receiving an average sale price of $274,900. Laundromats and dry cleaning services are also hot sellers, receiving an average sale price of $175,000.

Daniel used these showings to thoroughly qualify each candidate, first making sure they had the financial capability to make the purchase through a proof of funds letter. While some prospects wanted the business as an investment, one man came forward who wanted to run the bakery daily and even expand it. After three “very long” meetings going over the details, Daniel and Jenny agreed to sell in July, less than 30 days after listing the business for sale. The final sale price was $115,000.

Daniel credits the quick sale and successful price to a descriptive listing with attractive photos, providing a comprehensive package of information to buyers up front and being available to show the business right away. Some other tips sellers should consider for finding & narrowing down prospective buyers include:

- Does the buyer have the necessary capital? Ask prospects to complete a Personal Financial Statement, showing that they are able to secure financing and have enough capital to fund the down payment and the first year of operation.

- Does the buyer have the right business experience? A lack of previous ownership experience isn't always a deal-breaker. However, qualified buyers usually have business experience in the industry or a related field.

- Does the buyer’s timeframe align with yours? Talk to prospects early in the process to determine whether they are ready to pull the trigger on their ownership plans or whether they are still months or years away from making a serious offer.

- Is the buyer a long-term fit for your business? Evaluate whether the buyer’s skillset and mindset align with your customers, vendors and employees. Likewise, the prospective buyer's transition goals need to match yours, especially when it comes to your involvement with the company post-sale.

After the deal was signed, the transitional period started. Daniel quickly realized the most time-consuming part of the transition would be notifying his suppliers, partners and other vendors. From food suppliers and cleaning crews to billing help and the security company, everything in Daniel or Jenny’s name had to be changed. For each of his about 18 different vendors, Daniel had to fill out official change of ownership paperwork and ensure the new owner was aware of how each relationship worked. This included assuring each partner that the new owner would take care of the business and it would continue to be a mutually beneficial agreement between the parties.

Daniel and Jenny’s final job was to notify the employees. They waited until the day before the deal was done in order to ease concerns about job security. Daniel told them that a new owner would be coming aboard but emphasized that there wouldn’t be any significant changes.

“This was extremely tough because we were a small business and had become very close to our employees,” Daniel said. “When Jenny announced it, there were definitely some tears but we promised we would stay on for a month after the new owners took over to help make the transition go as smoothly as possible.”

Communicating a sale to employees can be one of the hardest part of a sale so it is important owners give it real thought beforehand. A few things sellers should consider before breaking the news:

- Not everyone needs to know about the ownership transition at the same time. Be strategic about communication before and during the sale process.

- Some key employees may need to be told before the deal is done- since employees may need to play a role in helping you prepare the company for the market or satisfy the due-diligence requests of a prospective buyer. Informing key employees early in the process also allows you to gauge their future intentions, and gives you time to incentivize them to remain with the business under a new owner.

- Give the news in person and provide employees with specifics about the new owner, the transition timeline, your reasons for selling, and other critical details. Express confidence in the new owner and in the company's future. Relay to employees just how much care was taken throughout the sale process to ensure the new owner is a good fit.

Like with many deals, Daniel & Jenny agreed to provide training for the new owners. Daniel said he and Jenny still have an emotional attachment to the bakery, so they took the training especially serious as they want it to continue to succeed. Even after the official training period ended, they remained available to answer questions from the new owners.

knowing how involved exiting owners should be in the business after the sale is an important issue to bring up during negotiations. In a recent BizBuySell.com survey, 48 percent of owners said they don’t want to be involved at all post sale. On the other end, just 18 percent want to be very involved, working at least 3 days per week. Buyers, however, typically enjoy the early help. In the same survey, 49 percent of prospective buyers said they want the previous owner working at least 3 days per week while just 11 percent said they want them completely uninvolved. With such a gap existing, both sellers and buyers need to make sure to communicate their needs early in the process to ensure they get what they need post-sale.

For Daniel and Jenny, their experiment as small business owners and as sellers was a success. They both have re-entered the real estate market. Daniel is actually using the bakery sale money to get a master’s degree to further his real estate career. It’s a great example of how small business owners can use a well-planned exit strategy to help fund their next endeavors in life.

As for reentering the small business market, Daniel and Jenny said they would consider it if they found the right fit.

“Owning a small business has many rewards but it was also one of the toughest experiences we have ever been through,” Daniel said. “We would definitely do it again, but only for a business type that we have a deep passion for. The first year especially requires countless hours of work so you really have to love what you are doing each day.”

Yesterday, we looked at concentration of small businesses— namely, the number of small businesses (1-99 employees) in a city expressed as a ratio per 100,000 residents of that city.

Today, we look at the percentage of private-sector jobs in cities that are generated by small businesses*.

Cities in California and Florida top this list, filling the first 5 slots and 7 of the top 10 — including No. 1: Santa Rosa, Calif.

Top 20: Where small businesses fill the highest percentage of private-sector jobs

1. Santa Rosa, Calif.: 48.7% of local private-sector jobs generated by small businesses

2. Sarasota-Bradenton, Fla.: 43.8%

3. Oxnard-Thousand Oaks, Calif.: 42.6%

4. Cape Coral-Fort Myers, Fla.: 41.2%

5. Daytona Beach, Fla.: 40.6%

6. Portland, Maine: 39.7%

7. Miami: 39.5%

8. Spokane, Wash.: 39.0%

9. Ogden, Utah: 38.6%

10. Fresno, Calif.: 38.3%

11. Providence, R.I.: 37.9%

12. Palm Bay-Melbourne, Fla.: 37.8%

13. Charleston, S.C.: 37.4%

14. New York: 37.3%

15. New Orleans: 37.2%

16. Portland, Ore.: 37.1%

17. Albuquerque, N.M.: 37.0%

18. Boise, Idaho: 36.9%

19t. Oklahoma City: 36.8%

19t. Bridgeport-Stamford, Conn.: 36.8%

Comments

Post a Comment